Why did you freeze it?

As mentioned earlier, the moratorium on the funded part of the pension was imposed due to the state’s need to generate additional income. Previously, defrauded investors decided to transfer the savings portion to non-state companies.

Now the amount is used to provide insurance benefits and other government needs. Another reason for suspending the program for forming the funded part of the pension is the planned indexation of payments for existing pensioners.

Expert opinion

Kurtov Mikhail Sergeevich

Practitioner lawyer with 15 years of experience. Specializes in civil and family law. Author of dozens of articles on legal topics.

The Russian government is trying to bring average monthly pensions closer to European standards. As a result, citizens will not be able to save on food, clothing and other needs.

Why was the “funded part of the pension” introduced?

The funded part of the pension was supposed to become an instrument that would provide a decent addition to the guaranteed insurance payment. It was assumed that citizens would not only be able to accumulate additional funds for old age, but would also multiply by investing. In the event of the death of a pensioner, the remaining funds were transferred by right of inheritance.

The accumulation of funds on long-term investments promised benefits in terms of economic development. The state received long-term money to finance long-term projects. People received an increase in savings through dividends from investments. Along with the Pension Fund, money can be entrusted to private investment funds.

Since 2008, the government has actively encouraged citizens to increase contributions to their personal accounts. For this purpose, a co-financing program was introduced:

- if a citizen voluntarily (and additionally) deposited at least 2,000 rubles into his account, then the state added another 2,000;

- per year the amount did not exceed 12,000;

- No restrictions were introduced for citizens.

The program was a success with the population. According to the Pension Fund of Russia, for example, in the Kemerovo region alone, by the end of 2014, people deposited about 484 million rubles into personal accounts.

What to expect regarding the moratorium on the funded part of the pension

It is already known what the state will do with frozen funds. They are used to fulfill the Pension Fund's obligations.

Economists argue that the moratorium will be extended several times. Initially, the pension freeze was planned for the end of 2013.

The action was intended to be a financial shock manipulation that would be applied at once. It was planned to be carried out in order to urgently support the Pension Fund.

The freezing of the funded part of the pension was implemented in 2014. However, the temporary measure was not enough.

Despite the fact that with the help of such an action the organization was able to receive almost 250 million rubles, the reserve still remained in a deficit state. This forced the government to extend the moratorium.

As a result, the freezing was extended for another 2 years. It is not yet clear when the funded part of the pension will be unfrozen. Experts say that there is no trend towards lifting the moratorium in 2021. The method paid off.

The organization was able to ensure an influx of funds. Experts believe that the reason for the severe shortage of funds is the illiterate management of pension policy.

The current system cannot be 100% applied in modern economic realities. Modernization needed.

Note! Resources received in the form of transfers to the insurance pension do not allow the fulfillment of the obligations of the Pension Fund. As a result, the government is forced to resort to distributing 6% of contributions to state needs.

Having figured out what freezing pension savings is, a citizen will find out that the implementation of the procedure entails the deprivation of additional income to citizens of the Russian Federation. They will not be able to profit from investments when they reach retirement age.

The measure was taken due to the fact that the Pension Fund is experiencing a lack of resources. In 2021, Law No. 413 came into force, which once again extended the moratorium on the funded part of the pension.

Expert opinion

Kurtov Mikhail Sergeevich

Practitioner lawyer with 15 years of experience. Specializes in civil and family law. Author of dozens of articles on legal topics.

From the above regulatory legal act it follows that the period will end at the end of 2021. If the next extension is not completed, the moratorium will be lifted.

Citizens will again be able to manage the funded part of their pension independently. However, there is no tendency to stop freezing.

Therefore, a repeated extension can be expected in the future.

The latest news says that the State Duma has approved another law extending the freeze on pension savings of Russians until 2021. All funds will again be used to form the insurance part.

As a result, citizens stopped receiving savings payments. To form this part of the pension, today you need to make voluntary contributions to a non-state pension fund or send maternity capital there.

The income of most citizens does not allow them to pay an additional amount to increase their pension in the future. Experts note that such an action is not a withdrawal of the accumulated portion.

She was simply frozen. In simple terms, the adoption of the norm deprives citizens of the opportunity to independently manage their pensions, increasing funds through the transfer of non-state pension funds.

The further fate of the funded part of the pension will be clear next year.

In 2021, the Government of the Russian Federation adopted Law No. 413-FZ of December 20, 2017, extending the freeze of the funded part of the pension. From January 1, 2021, contributions paid by the employer to the Pension Fund of the Russian Federation, which were then transferred to a non-state pension fund chosen by the citizen, are frozen again.

In this article we will take a closer look at what this means for ordinary pensioners.

Dear readers! Our articles talk about typical ways to resolve legal issues, but each case is unique.

How much will Russians lose from freezing the funded part of their pension?

We tell you what is happening to the pension savings of Russians

Photo: Svetlana MAKOVEEVA

This week, deputies again extended the freeze on the funded part of pensions - this time until 2024. This means that the personal accounts of Russians have not been replenished for 10 years. Let's figure out what this will lead to.

WHAT IS THE STORAGE PART?

The pension system in Russia is not simple. The amounts that older people receive now, and that we will all receive, consist of three parts:

- fixed part - the very minimum that the state guarantees to everyone

- the insurance part - is paid from the money that the employer contributed to the Pension Fund for the employee, depends on the length of service and is expressed in pension points

— the accumulative part is a personal increase in payments for each person.

The employer pays contributions to the Russian Pension Fund for his employee - 22% of the salary. Since 2002, when the next reform was carried out, 6% of them go to the funded part of the pension, and 16% to the insurance part. That is, in fact, into a common pot from which pensions are paid to today's elderly. A working person does not have this money, he only knows the number of his points. These points will turn into money only at the time of retirement: in 2021, 1 pension point is equal to 93 rubles, in 2024 it will be 116.63. What will happen next - no one knows, maybe less.

And the savings part is like a deposit in a bank. 6% from each salary drips into a personal account, where this money accumulates and makes a profit - due to the fact that a non-state pension fund or Pension Fund invests it. You can always see how much money has already flown in.

It is important to note that the funded part is formed only for those born in 1967 or later.

All indexations for pensioners concern only the insurance part of the pension

Photo: Svetlana MAKOVEEVA

WHAT PART OF THE PENSION IS INDEXED BY THE STATE?

Officials like to report that payments to elderly people have once again been indexed, that is, increased. The necessity and regularity of such a procedure are even enshrined in the Constitution.

But all indexations relate only to the insurance part of the pension - that from the common pot. The funded part grows due to the profits of non-state pension funds.

But it can be passed on by inheritance - unlike the money that was spent on the insurance part.

WHY WAS THE ACCUMULATIVE PART FROZEN?

This decision was made in 2014. Let us remember that then Crimea returned to Russia, for which our country was subject to sanctions. The times were difficult: the authorities needed not only to fulfill all their obligations, but also to invest money in the development of the peninsula. In addition, more and more people were going on well-deserved retirement, and there were fewer workers. That is, there were too few people who would throw themselves into the common pension pot.

Then they decided to temporarily transfer 6% of insurance contributions to the insurance pension. This made it possible to reduce the hole in the Pension Fund’s budget, but not close it - it receives subsidies from the budget every year.

As a result, millions of people were left without potential savings and income (more on this below), and the Russian economy lost a powerful source of financing, because NPFs are a classic investor in large projects with a long payback period.

It is possible to calculate how much you lost from freezing the funded part of your future pension

Photo: Svetlana MAKOVEEVA

WHAT HAPPENED TO THE MONEY THAT WAS SAVING UNTIL 2014?

They haven’t gone anywhere—they remain in your account and generate income. There are no new deductions there, but no one confiscated the previous ones.

Everyone has the right to choose a fund that will manage their savings. If you have not done this, the Pension Fund is looking after you. He sends the money of the “silent people” to the Management Company of Vnesheconombank.

HOW DO I FIND OUT HOW MUCH I HAVE SAVED?

The easiest way to do this is on the State Services portal - just order an extract on the status of your personal account from the Pension Fund of Russia. If the money is kept in another fund, find out which one and make a request there.

IS IT POSSIBLE TO CALCULATE HOW MUCH I HAVE LOST?

Understanding the domestic pension system is not easy, let's try to do this with an example. Let's take the conditional Russian Alexander Ivanov. His life is stable, his job does not change, he receives 50 thousand rubles a month.

The employer pays 11 thousand rubles in contributions per month to the NPF for Alexander. If it were not for the freezing of the savings part, 3 thousand of this amount would have gone not into the general pot, but into Alexander’s personal account. For a year this is 36 thousand rubles. And in the 10 years that the freeze will be in effect (we still cannot know what decision the authorities will make after 2024), 360 thousand would have flown in, respectively.

Any reader can substitute his salary here and calculate how much another annual extension of the current scheme costs him personally.

But this is not all our losses. After all, a funded pension doesn’t just sit somewhere in a safe and accumulate. Pension funds invest this money and earn money for their investors. It turns out that they are not doing very well: rather, they are helping to save money from inflation. Since 2014, when the funded part of pensions was frozen, the average return on non-state pension funds has been 7.4%.

This means that at the end of 2019, our Alexander Ivanov did not receive 63,376 rubles of investment income into his pension account. And by 2024, he could become richer by another 121,622 rubles. Of course, these are conditional calculations, because we do not know what kind of profitability this or that NPF will show in the future.

For clarification about your future pension, you can contact the Pension Fund branch or go to the State Services portal

Photo: Maria LENZ

WHAT HAPPENS IF THE ACCUMULATIVE PART IS DEFROSTED?

Our savings will begin to grow rapidly again. Then, perhaps, it will be possible to accumulate a significant increase in pension. Because the more than 4 trillion rubles that are now circulating in this system will not be particularly noticed by Russians in the form of pensions; it is too little per person. Moreover, you need to take into account that from the accumulated amount I will pay you a monthly bonus, and will not give it entirely to you. Payments will be calculated based on the survival period - the time that the average Russian lives in retirement. Now it is 258 months.

By the way, no one is prohibiting increasing pension savings even now. You just need to conclude an additional agreement with your fund and transfer money there directly.

MORE ON THE TOPIC

Deputies extended the freeze on the funded part of pensions: what does this mean?

All contributions will go to the insurance part until 2023 (details)

Reasons for introduction in Russia

The freeze (moratorium) of compulsory pension provision (insurance) negatively affects the future income of citizens of the Russian Federation who are officially employed and hope to receive a decent pension. Investing the funded part of a pension at the expense of a non-state pension fund increases the amount of contributions to 100% , while investors do not suffer financial losses and are not required to pay additional funds to the fund.

The obligation to pay all contributions lies with the employer, and the citizen can choose their future fate: leave the funds for distribution and their further payment to current pensioners, or transfer them to savings for the purpose of generating income in the future.

But the moratorium does not allow citizens to 100% exercise their right to choose their future pension . NPF clients who decide to increase the size of future pensions using private fund funds are forced to put up with the new Law of the Russian Federation, which limits their formation.

This is important to know: Begging: article of the Code of Administrative Offenses of the Russian Federation

According to the Law, during the introduction of a moratorium on the formation of the funded part of pensions in the Russian Federation, all contributions from depositors are forcibly distributed to the insurance part.

The introduction of the moratorium is due to the presence of financial problems in the country's budget. In particular, the Pension Fund of Russia, which makes payments not only of a pension nature, but also for social purposes, receives a shortfall of up to 1.2 trillion.

rubles annually. The shortage is due to the unscrupulous activities of thousands of Russian employers who continue to pay wages “in envelopes” or delay the transfer of funds to the budget.

The shortage of funds in the Pension Fund is forcing the Government to look for new ways to obtain finance. Freezing the funded part of the pension provides a profit of more than 500 billion rubles , which help the fund fulfill its obligations to Russians.

Why is that?

In 2002, Russia moved to a more progressive and fairer pension model. But, as often happens, it turned out that “there is no money.” And instead of people increasing their future pension by creating a funded part, they transfer all their contributions to current pensioners.

To understand the scale of the problems with the Russian Pension Fund, it is enough to recall two important events related to pensions that occurred several years ago.

- From 2021, the Russian government has abolished the indexation of pensions for working pensioners (indexation occurs only after dismissal). That is, if you work, then you get paid normally, if you quit, then we will increase the size of your pension.

- From 2021, a new pension reform “2019-2028” began to work, within which the retirement age will increase from 55 to 60 years for women and from 60 to 65 for men. That is, pensions will begin to be paid later, which will lead to two logical consequences: people will make more contributions to the Pension Fund (since they will work longer) and will receive less money from the Pension Fund (since they will have less time to retire).

After this, is it really worth being surprised at the extension of the freeze on the funded part of the pension?

Why are savings frozen?

Freezing the funded part of the pension allows the state to receive additional income from the funds of investors who transferred their savings to a non-state company. Their funds will continue to be allocated for the insurance portion and distributed for government needs.

One of the reasons for the suspension of the compulsory pension insurance program is the constant planned indexation of the size of pensions for existing pensioners (read about insurance of the funded part of the pension in our article). The Government of the Russian Federation plans to bring the average monthly pension of Russian citizens closer to European standards , allowing pensioners not to save on food, clothing and other needs.

But for future retirees who are currently working citizens of the Russian Federation, such amendments to the legislation incur certain financial losses. On average, a working Russian with a salary of 30 thousand.

Expert opinion

Kurtov Mikhail Sergeevich

Practitioner lawyer with 15 years of experience. Specializes in civil and family law. Author of dozens of articles on legal topics.

rubles for his work experience will be able to provide a reserve consisting of savings funds indexed by a non-state fund in the amount of up to 2 million rubles.

These funds will be used to increase his future pension. The freeze prohibits Russians from increasing their income through the OPS program .

The only option for co-financing remains joining programs that provide for independent contributions to NPFs, for example, individual pension plans.

What will happen next?

Consequences, expectations, forecasts It is legally stipulated that the freeze on the funded part of the pension has been extended until the end of 2019 . At the same time, Russians who transferred their transfers after the start of the moratorium (January 1, 2014) will not be able to receive income from non-state companies for the period of the freeze.

What will happen to the part that the state froze is known: it will be used to pay off the obligations of the Russian Pension Fund. At the same time, according to economists’ forecasts, the moratorium will be extended several times.

At the same time, initially the pension freeze, which first occurred in 2014, was planned at the end of 2013 as a one-time event of a “shocking” financial nature, implemented for emergency economic support of the Pension Fund.

However, one-time measures turned out to be insufficient: despite the influx of capital into the Pension Fund in the amount of almost 250 billion rubles in 2014, the reserves for the next year remained in a deficit state. This forced the Russian Government to extend the moratorium until 2021; later the freeze was extended again for 2 years.

There are no trends towards lifting the moratorium in 2021 yet : the measures taken to increase the influx of financial resources by freezing the funded part of the pension are paying off. Some experts believe that the reason for the lack of finances in the Pension Fund is the unjustified strategy for creating pensions in the Russian Federation, which cannot yet be 100% applied to the peculiarities of the Russian economy.

Freezing the funded part of the pension deprives Russian citizens of receiving additional income upon reaching retirement age. The measures taken by the Government of the Russian Federation are due to a lack of resources in the Pension Fund.

In 2021, Law No. 413-FZ of December 20, 2017 was adopted. on extending the moratorium until the end of 2021. There is no tendency yet to lift the freeze on the accumulated portion of Russians’ pensions.

Didn't find the answer to your question? Find out how to solve exactly your problem - call right now:

Freezing the funded part of pension savings is one of the most important stages of modern pension reform. If earlier citizens could independently decide how their material security would be formed in old age, today this possibility no longer exists. The reason was the temporary cancellation of the funded pension.

What is freezing?

Freezing the funded part (hereinafter referred to as NP) leads to the fact that 6% of payments that the employer transferred to the Pension Fund are no longer stored in the personal account of the insured person, and the state uses these funds at its discretion.

According to preliminary calculations, thanks to the freezing of low frequency, the federal budget will be replenished by 400 billion rubles in 2021.

The authorities promise to take into account part of the lost funds in the form of points upon retirement, which will completely depreciate by retirement age or the pension reform will change again.

But why didn’t the reform to introduce the funded part work?

LF has been introduced since 2002. Savings were formed by citizens born in 1967 and younger. The percentage of deductions was 6%.

Every citizen who had savings could transfer these funds to a non-state pension fund (non-state fund) or to a management company (management company), where the profitability is higher than in the state-owned Vnesheconombank.

It is important to know! Pension payments to former employees of the Federal Penitentiary Service

However, the financial balance of the Pension Fund began to go negative. Therefore, in 2014, the Government decided to freeze NPs.

For what reasons did this happen?

In 2014, in connection with an audit of the activities of non-state pension funds, the Government decided to freeze funded pensions for 1 year. The moratorium was extended into the next year, but for other reasons. The freeze was extended due to the unstable economic situation in the country.

Due to the financial crisis, the federal budget began to experience a shortage of funds for payments to existing pensioners (they were formed from insurance contributions). In this regard, it was decided to temporarily suspend the new system.

- The 6% that employers contributed to the NPF will again be used to create an insurance pension;

- all contributions to the Pension Fund of the Russian Federation will be used for current payments to state employees and pensioners;

- Funds from the funded portion will not be invested into non-state pension funds during the moratorium, which means their growth will stop.

This will help put the balance of the state treasury in order, resolve a number of social problems and stabilize the economic system.

Freezing the funded part of pensions - who is affected?

First of all, the freezing of funded pensions directly affected those categories of citizens born after the end of 1967, since previously only they had the full right to the funded part of the pension benefit. On the part of the employer, there is a deduction to the Pension Fund for each employee of the organization of about 22% of his salary. Of the total amount, 16% is given directly to the solidarity part, in order to then become directly the insurance part of the pension provision. In other words, these are a kind of virtual funds for citizens, which from next year will be converted into points, and it is from these that the amount of pension benefits will be calculated in the future. In the future, these funds will be indexed twice during the year, which is associated with a high level of inflation. For those employees of organizations who were born before 1967, 22% of the funds are spent on this.

Contribution "ICB. Practical" Moscow Credit Bank, Lit. No. 1978

up to 6.25%

per annum

from 50 thousand

300 days

Make a contribution

For how long was the formation of the NPP cancelled?

The decision to temporarily cancel the formation of the funded part was made on 4.12. 2013 on the basis of Federal Law No. 351. The law came into force in 2014. From that time on , it was decided to again direct all pension contributions to the formation of the insurance part . Contributions began to flow into the Pension Fund for current payments to pensioners.

Expert opinion

Kurtov Mikhail Sergeevich

Practitioner lawyer with 15 years of experience. Specializes in civil and family law. Author of dozens of articles on legal topics.

Initially, the Government assumed that it would be frozen for 1 year, but due to the discrepancy in the balance of the federal budget caused by the worsening crisis, on December 1, 2014 it was decided to extend it. It was then extended in 2015 and 2021.

The main question that concerns citizens, about how long the funds will be frozen, remains unanswered. At the moment, the Government plans to extend the moratorium until 2019.

This is important to know: Exemption from payment of state duty: petition, who is exempt from payment by law

Pension results for 2014: no savings left

In whose hands are future pensions?

Another, no less significant risk for the pension industry is the high concentration of assets. 2014 can rightfully be called the year of pension M&A. On Thursday, December 25, one of the largest transactions on the market was completed: Boris Mints’ investment holding O1 Group acquired 100% of the shares of NPF Blagosostoyanie OPS. In addition, O1 Group controls NPF StalFond and NPF Telecom-Soyuz. The total assets of funds managed by the company exceed 154.6 billion rubles, and the number of clients is 2.8 million people. At the end of November, it also became known that the structures of banker Anatoly Motylev acquired the NPF Sberfond RESO, whose assets amounted to 16.3 billion rubles.

Read on RBC Pro

Nassim Taleb - RBC: “I see a threat more serious than a pandemic”

Why Amazon creates failed products and what's wrong with their design

How 12 startups are revolutionizing global finance

When China will become the world's first economy: 5 scenarios from Bloomberg

During 2014, several more transactions for the sale of large NPFs were closed on the market, as a result of which a significant part of the NPF savings came under the control of several financial and industrial groups. Among them is the Otkritie group, whose structure includes NPF Elektroenergetiki and NPF LUKOIL-Garant, co-owner of B&N Bank Mikail Shishkhanov, former top manager of AFK Sistema Evgeny Novitsky, structures of the already mentioned banker Anatoly Motylev, as well as the group funds whose activities are related to Gazprom.

The consolidation of pension assets in the hands of several businessmen did not go unnoticed by the regulator. Therefore, the Central Bank decided to limit the ability of non-state pension funds to invest in companies of the same group. As Philip Gabunia said, funds will be able to invest no more than 25% of assets in affiliated companies, while NPFs will be able to invest up to 10% of assets on deposits of banks included in the group.

True lies: how officials promised to save spent pensions Photo gallery

From freezing to liquidation

Since the deputy chairman of the Pension Fund, Nikolai Kozlov, speaking at a conference in Khanty-Mansiysk in October 2014, informed everyone that the state would not have the funds to create mandatory pension savings for citizens for another five years, it would seem that nothing indicates that that the government may decide to dismantle the pension system. At the same time, the situation in the Russian economy is getting worse and worse. As the head of the Ministry of Economic Development Alexey Ulyukaev admitted on Tuesday, December 23, the macroeconomic forecast for 2015 will have to be adjusted. According to the latest forecast of the Ministry of Economic Development, Russia's GDP will decrease by 0.8% in 2015. According to Finance Minister Anton Siluanov, due to declining revenues, the budget deficit in 2015 may be significantly higher than the planned 0.6% of GDP.

This may force the authorities to again resort to a method of saving that has been tested by the authorities: the withdrawal of employer contributions transferred to the funded part of the pension in favor of the Pension Fund. At the beginning of December 2014, Russian President Vladimir Putin signed a law extending the moratorium on the transfer of pension savings to management companies and non-state pension funds until 2015. As a result, future pensioners for the second year in a row did not receive money into their savings accounts, but budget expenditures to cover the Pension Fund deficit decreased by 307 billion rubles. In 2013, due to a similar maneuver, the authorities saved 243 billion rubles, however, these funds were frozen and will be returned to the funds that will be included in the guarantee system in 2015. All this money went to current payments to pensioners. Future pensioners and the Russian economy as a whole lost: after all, if not for the “freeze”, this money would have been invested in shares and bonds of companies. Perhaps this would have made it possible to avoid a crisis in the debt borrowing market and, as a consequence, to avoid losses of the NPFs themselves.

The likelihood that funds will be forced to record losses at the end of the year is very high, since many have invested in debt instruments. OFZs are now trading below par, and defaults have begun on the corporate debt market. In early December, UTair defaulted on its exchange-traded bond offer. The share of the airline's securities in the portfolios of non-state pension funds is estimated at 5%. Pension money managers do not yet know how to write off this loss.

The issue of low returns compared to inflation, which are shown by management companies and non-state pension funds, has always been one of the main arguments for representatives of the government’s social block who advocated the abolition of pension savings. If their point of view prevails, then next year we can expect a return to the distribution scheme for pension payments.

What will happen to the funds?

According to Deputy Minister of Labor Andrei Pudov, the accumulated pension funds have not gone away after the adoption of the moratorium law. People who will retire soon will be able to receive this money.

We talked about whether it is possible to withdraw the funded portion before retirement, in a separate article, and you can find out whether working pensioners can apply for it here.

The freeze does not reduce the pension rights of citizens and does not mean the abolition of the funded system. It turns out that the 6% that the employer contributed monthly to the non-state pension fund, as well as investment income from these contributions, still remains with the owner of the pension account.

In their opinion, during the moratorium, citizens will not lose the funds that formed the monthly savings part, but will lose the projected investment income from them.

It turns out that the state guarantees the return of the funded part, but does not compensate for the loss of possible investment income that citizens would receive by keeping their savings in partner banks of the Pension Fund of the Russian Federation and Non-State Pension Funds.

Those Russians who retire have the right to return their savings in several ways:

- One-time payment . It can be received by disabled people, pensioners, as well as citizens whose savings amount is less than 5% of their old-age pension.

- Urgent payment for 10 years . Reliable to those who formed a pension through voluntary contributions.

- Lifetime. Assigned if the amount of savings is more than 5% in relation to the amount of old-age payments.

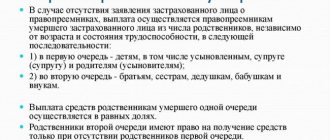

- By inheritance. Entitled to the relatives of the deceased owner of the personal account by law or will. Paid in one lump sum. We tell you more about whether and how to receive the funded part of the deceased’s pension here.

Despite the temporary abolition of this system, citizens have the opportunity to increase material security in the future using the co-financing program . You can become a participant in this program until December 31, 2015.

Such a system, unlike a funded system, involves independently depositing money from your personal budget.

The moratorium entailed a number of consequences: an increase in interest rates on loans for the population, an unstable situation in the work of non-state pension funds, as well as the loss of possible investment income by citizens. Nevertheless, the current moratorium does not deprive citizens of the right to receive pensions, including the funded part (read about payments under the funded part here).

Video on the topic

The “freeze” of pension savings was introduced in 2014 due to the budget deficit of the Russian Pension Fund. Since then, it has been extended several times until the final decision was made to eliminate the old pension savings system by 2021.

Of course, it should be replaced by a new one, the bill of which has not yet been made available to the general public.

At the end of November 2021, a new bill to extend the “freeze” was approved by 316 deputies out of 408. The President also approved Law No. 462-FZ, signing it on December 11.

The legislative act came into force at the beginning of 2021. Of course, the new reform has reduced the already shaky confidence in the Russian pension system, but it will solve the problem of the Pension Fund budget deficit, which increased 2.4 times in 2021.

It is planned that by 2021 the budget deficit will decrease by 29.2 billion rubles.

Why was “freezing” needed?

Previously, residents of the country could form both insurance and funded pension payments. This happened due to contributions from their employers, amounting to 22%. 16% of them went to form an insurance pension, 6% - to a funded pension.

Since 2014, all 22% began to be used to create rights to insurance payments, and the funded part of pensions was “frozen”. This means that the savings that have already been transferred to the NPF have not gone away, but now they are growing only through the bank’s investment of stored funds.

The amount accumulated by the pensioner still belongs to him, but he himself can no longer replenish it.

- By the end of 2013, the Pension Fund announced a budget deficit. This means that the level of fund expenditures significantly exceeded the level of incoming funds.

- On December 4, 2013, corresponding amendments were made to Law No. 167-FZ - the government “froze” the funded part of pensions. It was initially planned that the moratorium would not last long.

- However, in 2021, a new freeze period was adopted: from 2021 to 2021. And at the end of last year, by a final decision, the deadline was extended for another year.

The “freeze” made it possible to continue paying pensions to those who had already retired. According to M.A. Topilin, Minister of Labor and Social Protection, this measure helped save the budget over two trillion rubles. Lawmakers believe that thanks to the moratorium, 609.1 billion rubles will be saved by 2021.

What is freezing a funded pension?

As mentioned above, 22% is divided into 16% (the insurance part of the pension) and 6% (the funded part of the pension). But that's just how it should be

be. Since 2014, the government has been “freezing” the funded part of pensions. This means that all 22% goes to the insurance pension, that is, all the money that the employer pays for the employee goes to citizens currently receiving a pension. And you can forget about the 6% that should go to him personally and multiply (increase due to the investment activities of the Pension Fund or Non-State Pension Fund).

In mid-December 2021, another “freeze” of the funded part of the pension occurred. According to the document (Federal Law No. 405-FZ dated December 8, 2020), it will last at least until 2023. The freeze includes exactly the same 6% that the employer pays (there are other ways to replenish the savings portion).

The future of the savings system

The moratorium will no longer be lifted, since the pension savings system has shown itself to be insolvent. Already in 2014, the development of a new program began that could replace it.

Thus the IPC system was born. It implies that a person decides for himself how much and for how long to save for a future pension.

Its launch was scheduled for 2021, but due to the new reform regarding raising the retirement age, it was decided to postpone the innovations until 2021. Starting this year, people will be able to open an IPC account and deposit as much money as they wish.

The state will be able to help citizens create savings using tax deduction amounts (including social). Employers will also be able to take part in increasing the pension capital of their employees, in return receiving some benefits from the state.

Those who have accumulated savings by this time will be able to transfer them to the new system. The funds will be paid in the form of an additional pension. In some cases, the account holder will be able to receive the money before a certain age. At the same time, each participant in the new program will be able to leave it if they wish.

Truth and fiction

Expert opinion

Kurtov Mikhail Sergeevich

Practitioner lawyer with 15 years of experience. Specializes in civil and family law. Author of dozens of articles on legal topics.

There is an opinion that the “frozen” savings of Russians will disappear along with the previous savings system. This is a common myth that still scares people.

“Freezing” does not mean at all that those funds that have already been generated will not be paid. They just stopped increasing due to contributions from employers.

Anyone who has accumulated an amount in a non-state pension fund and has also reached a certain age can apply for payment of their savings by choosing the most convenient way to receive them.

Until 2021, only those who had reached the age of retirement could receive this type of pension payment (this age was raised by the reform). However, for receiving savings it remains the same and is 55 years (for the female population of the country) and 60 years (for the male population).

This is important to know: Returning wallpaper to a store: legal actions

V. Putin extended the freeze on the funded part of pensions until 2022

On December 16, 2021, President V. Putin signed Law No. 435-FZ. It provides for the extension of the moratorium on funded pensions until 2022 instead of 2021, as was previously established.

Such a moratorium was first introduced in 2014 due to the Pension Fund’s budget deficit. At first this decision was considered temporary, but subsequently the moratorium was constantly extended. Coming in 2021

a decision was made to “freeze” until the end of 2021, then it was decided to extend this for another year - until 2021. Now the issue has been returned to again to extend the moratorium until 2022.

What does “freezing the funded part of a pension” mean?

Recently, future retirees have begun to actively transfer their pension savings to non-state pension funds (NPFs), which promise to create a reliable investment portfolio that will generate profit, thereby increasing their future pension. The flexibility of conditions, payment schedules, contribution amounts, as well as the possibility of appointing an heir made NPF programs attractive.

However, the Government recently announced the suspension of the transfer of funded pensions to private funds, which worried the people. For 2 years now, savings have not been sent to any non-state pension funds, since the authorities are creating the insurance part of the distribution pension system. And for this, the state needs all insurance contributions transferred by employers in accordance with the terms of the compulsory pension insurance program for employees.

- persons whose date of birth falls before 1966;

- male population born in 1953;

- female population born in 1957.

- 16% from the salary amount to be used to form the insurance part of the pension benefit;

- 6% will be allocated to the formation of the savings part, 10% to the insurance part.

If the citizen did not declare his choice, the first option was automatically applied. The so-called “freeze” of the funded pension affected persons born later than the beginning of 1967, for whom contributions to the Pension Fund are made by the employer, acting as an insurance agent.

In total, 22% of funds are withheld from wages, of which 16% is transferred to increase the insurance part of the pension, 6% to the funded part. And the “freeze” has led to the fact that all 22% now goes to the insurance part, and the formation of the savings part has stopped.

What is the funded part of a pension, and why is it needed?

In 2002, a pension reform was carried out, within which the pension was divided into two parts - insurance (compulsory) and funded. The insurance is a fixed amount, which the state periodically indexes (increases). A funded pension is a supplement to the pension that citizens should receive.

The employer contributes 22% of his official salary for each employee. 16% goes to the insurance part of the pension and is paid to people who are pensioners right now. And 6% goes to the funded part of the pension - this money is put aside in a special account, where it is not just kept, but invested, so in the end the amount should be even larger.

There are various factors like length of service, etc., that affect the size of the insurance pension, but it is the same, plus or minus. Some have 14 thousand, some have 16 thousand, some have 19. Yes, there is a difference, but it is not that colossal. The point is in the calculation system - it smooths out the difference and makes pensions approximately the same.

The funded part of the pension was supposed to improve the situation - the more a person (his employer) contributed to the pension fund, the larger his pension should be. And he himself will receive the insurance part of the pension (new generations will pay it) and the funded part of the pension (the money that he earned and saved, and the Pension Fund or Non-State Pension Fund increased their amount). It seems logical. But something went wrong...

Differences between insurance and funded pensions - what you should know

Funded and insurance pensions have significant differences between themselves. You should be aware of this when deciding on the priority in the formation of one of them:

- Insurance contributions towards the insurance pension are converted into “pension points”. The funded pension is calculated in real money.

- The insurance pension is not inherited by legal successors.

- No one manages the savings in the insurance pension account; this money is not invested anywhere. Its size depends on inflation - it is indexed annually. The funded pension is placed at the disposal of a management company or private pension fund, it is invested - the funds are multiplied thanks to the profits from the investment portfolio.

- Funds received in the form of insurance contributions to accumulate an insurance pension are paid to citizens of the country who have reached retirement age. The funded pension is invested in stocks, bonds, enterprises and “works”, bringing profit - this money is not paid to the country’s pensioners.

- The funded pension can be increased by making additional voluntary contributions. This procedure does not work with an insurance pension.

- A funded pension can be received as a lump sum payment if the amount of savings does not exceed 5% of the total pension. It is not possible to receive an insurance pension “at once”.

Common mistakes

Error: A worker, having decided to calculate the number of accumulated pension points, takes into account insurance contributions for the formation of both an insurance and funded pension.

Expert opinion

Kurtov Mikhail Sergeevich

Practitioner lawyer with 15 years of experience. Specializes in civil and family law. Author of dozens of articles on legal topics.

Comment: Only contributions to the insurance pension are subject to transfer to “individual pension coefficients”, since this money will be used to pay pensions to other pensioners until the contributor himself reaches retirement age.

Error: “Freezing” the funded pension will result in citizens receiving a refund of contributions from the NPF made before 2014.

Comment: Deposits in non-state funds will remain untouched if the money was invested before 2014.

To be or not to be pension savings

The benefit, according to the next pension reform, should consist of several components:

The latter was to be formed from the personal savings of citizens. However, due to recent changes in the country's economy, state financial policy has also changed.

The funded part should be formed taking into account the period of work of the future pensioner and the amount of his salary. The amount of deductions sent to a person’s personalized account depends on these parameters.

It is theoretically possible to use such savings in various ways:

But she will not be able to use this money until 2021. The moratorium on freezing the funded part of the pension has been extended until 2021.

Will there be a funded part of the pension or not?

Since 2002, a pension reform has been carried out in Russia, as a result of which the pension began to consist of different parts, namely:

- insurance;

- cumulative.

These innovations applied only to citizens who were born after 1967. The funded part was initially planned to be allocated from the personal funds of future pensioners. It was supposed to depend on length of service, as well as salary. The use was supposed to be implemented as follows:

- by transferring money to a non-state pension fund, which will begin to increase it and assign interest on financial transactions carried out;

- investing in the Central Bank, mortgage programs and bonds;

- receipt in shares or a lump sum, as well as transfers for the purpose of improving health or living conditions.

However, the difficult economic situation in the country forced temporary amendments to the legislation, namely, the introduction of a moratorium on the funded part of the pension. Currently, this measure has been extended until 2021. Until this time, it will not be possible to use the accumulated money, with few exceptions.