Fixed payment

According to the Law “On Insurance Pensions”, a fixed payment is a part of the pension that is accrued in addition to the insurance premium and does not depend on the amount of insurance premiums paid. It is issued to every Russian citizen of the appropriate age as a bonus. The amount of this payment is fixed and equal to 5,334.19 rubles (as of 2021). The exceptions are residents of the Far North, orphans, disabled people and other beneficiaries (the full list is given in Law No. 400-FZ “On Insurance Pensions”). They can count on an increased fixed amount.

Pensions for working pensioners in 2021

In 2021, the government decided to cancel the indexation of benefits for working pensioners. Although there was an increase in payments to this category of pensioners due to contributions from employers and accumulated IPC.

READ ON THE TOPIC:

A survivor's pension will be assigned for each deceased son or daughter.

Now a citizen of retirement age will be able to obtain the right to indexation by terminating all employment relationships.

In addition, the benefit will be recalculated taking into account all increases that occurred during employment. Parliamentarians discussed the issue of completely abolishing payments in favor of working pensioners, but did not make a final decision.

According to experts, pensions for working pensioners will most likely not be abolished in 2021; citizens will be able to continue to receive pensions and salaries at the same time. There is also no clarity regarding the future recalculation of benefits. Most likely, next year workers’ pensions will also not be indexed.

New amendments made to the Federal Law “On Insurance Pensions” deprived working pensioners of the right to an annual increase in payments. At the beginning of February, indexation affected only the benefits of non-working citizens of retirement age.

Working pensioners can increase benefits in other legal ways:

- over the course of a year of work, the total number of points will increase by a maximum of 7.83;

- Every year on February 1, the cost of one point increases;

- increasing the size of the fixed part of the pension.

Each parameter can have a significant impact on the size of the benefit, and the pension can be increased even more than with indexation.

The repeal of the amendments to the pension law does not seem to be in sight. In any case, the restriction will last at least until February 1, 2021. And then, if the economic situation in the country stabilizes, it is quite possible that this restriction will be lifted.

Insurance pension

This is part of the pension that is paid to a citizen every month as compensation for wages and other payments that he stopped receiving after he stopped working. What are the conditions for payment? This is influenced by age, occupation, length of service and the presence of a minimum amount of pension points.

Those who simultaneously fulfill the following conditions can count on an old-age insurance pension: 1. Reached the age of 61 years (men) or 56 years (women) - from this year in Russia they began to gradually raise the retirement age to 65 and 60 years, respectively. However, for those who were supposed to retire this year - men born in 1959 and women born in 1964 - there is a relaxation: in fact, the retirement age for them will be increased by six months. But there are exceptions: some preferential categories of citizens can retire early. But municipal and civil servants will have to stay at work late. The retirement age of officials will increase from 2021. In 2019 it is 56.5 and 61.5 years, respectively. 2. Have officially worked for at least 10 years (relevant for 2021, this figure will increase in the future). 3. Accumulated at least 16.2 pension points (valid for 2021, will also increase over time). This amount depends on the amount of insurance premiums paid during work. If a person has not accumulated the required length of service or has not accumulated the minimum number of pension points, he will not be granted an insurance pension. Early granting of a pension (for example, if a person worked in hazardous conditions or in the Far North, was a teacher or a doctor) may be refused if special experience has not been developed and there are no documents confirming the nature of the work and earnings. Oksana Krasovskaya, leading lawyer of the European Legal Service

What is it made up of? The insurance pension consists of several parts: Part of the insurance pension earned before 2002. Part of the insurance pension calculated for the period from 2002 to 2014. Part of the insurance pension earned after 2015. Part of the insurance pension accrued for other (non-insurance) periods. From 2015 to the present, the amount of the old-age insurance pension in each period is affected by the individual pension coefficient (IPC), which is calculated in points. Knowing it, you can calculate the expected pension amount in rubles. Old-age insurance pension in rubles = IPC × value of the pension point on the date of assignment of the insurance pension + fixed payment on the date of assignment of the insurance pension For 2021, this formula will be as follows: Old-age insurance pension in rubles = IPC × 87.24 rubles + 5,334, 19 rubles

The size of social pensions in the Russian Federation

| Category of pension recipients | Pension amount |

| 4959.85 rubles per month |

| 11903.51 rubles per month |

| 9919.73 rubles per month |

| 4848.29 rubles per month |

IPC until 2002

The value of the coefficient in this period is influenced by three parameters: Length of work experience until 2002. The average official monthly salary for 2000–2001 or for any 5 years before January 1, 2002 (here you need to choose which is more profitable). Length of work experience until 1991. The size of the pension in rubles depends on the accuracy of the assessment. But there is a nuance here: the Pension Fund does not have all the data on citizens for this period. Therefore, when calculating the coefficient using an online calculator, you will most likely get an approximate value. If you decide to challenge it, you will have to recalculate everything yourself (there is a detailed algorithm) and provide a package of documents to the Pension Fund.

How pensions will be indexed in 2021

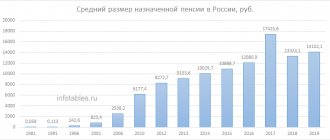

Russian Prime Minister D. Medvedev recently called on the governing bodies of the state and employees of leading departments to make every effort to return to the normal schedule for indexing pension payments. He said that the current situation with the increase in benefits has led to a loss of the purchasing power of pensions, and only by returning to the procedure for recalculating benefits stipulated by the legislation of the Russian Federation, can this situation be changed. The head of government then demanded that this order be restored from 2017 and that payments be returned to their size and capabilities.

According to Medvedev, the state's economic problems should not affect assistance to older citizens. He supported the proposals of regional authorities to provide single veterans and disabled people of the Second World War with free social assistance at home. But when asked whether pension reform will be carried out in 2021, the prime minister did not answer.

IPC after 2015

The value of the coefficient in this period is affected only by the amount of insurance premiums that were transferred on behalf of the employee.

The standard amount of such contributions is different for each year, therefore the coefficient is calculated separately for each year. These values are then added together. For manual calculations, you can use simplified formulas that give a fairly accurate result: IPK 2015 = average monthly salary in 2015 / 59,250 × 10; the maximum value is 7.39. IPK 2021 = average monthly salary in 2021 / 66,333 × 10; the maximum value is 7.83.

IPK 2021 = average monthly salary in 2021 / 73,000 × 10; the maximum value is 8.26.

IPK 2021 = average monthly salary in 2021 / 85,083 × 10; maximum value - 8.7

IPC 2021 = earnings for 2021 until retirement × 0.16 / 184,000 × 10; the maximum value is 9.13.

Indexation of pensions in 2016

READ ON THE TOPIC:

From August 1, 2021, pensions for working pensioners have been increased, and in 2021 pensions for non-working pensioners will be fully indexed.

This issue was actively discussed by interested departments and the public in 2015-2016. The economic situation in the country does not allow for a standard recalculation of payments in favor of pensioners, that is, increasing benefits to the real inflation level. Deputies and high-ranking officials proposed different ways to solve the problem. As a result, they decided to index insurance pensions by only 4%, which was done on February 1. The question of a second wave of increases was not raised at all. Some time later it became known that additional indexation was possible in the fall,

but a caveat was also voiced: the percentage of indexation would depend on the economic state of the state.

The government promised that the decision on indexation could be made in the summer of this year, and its size could be a percentage equal to the inflation rate.

IPC for other periods

Others include socially significant periods in the life of each person. This could be military service or caring for a newborn. Each period has its own coefficient, the value of which is determined in the Law “On Insurance Pensions” No. 400-FZ. So, for a mother or father who cared for the first child, or a man who served in the army, the IPC value will be 1.8. For one of the parents who cared for the second child, the coefficient will be 3.6. The total value of the IPC for other periods is equal to the sum of the coefficients for each such period of time separately. The calculation in this case can also be done using an online calculator.

Cumulative part

A funded pension is an amount that is formed in the employee’s personal bank account and consists of insurance contributions from the employer.

After retirement, the citizen receives part of this money every month or once the entire amount. Only those who are officially insured and have the right to an insurance pension can count on a funded pension. The following citizens will be able to receive the funded part: Those who were born in 1967 and later, officially work and for whom the employer pays insurance premiums to finance the funded part of the pension. A man born from 1953 to 1966 and a woman born from 1957 to 1966, for whom the employer paid insurance contributions to the funded part of the pension from 2002 to 2004. A woman who transferred maternity capital to the funded part of her pension. Anyone who participates in the State Pension Financing Program. The funded part can be calculated using the formula: Funded pension = total amount of pension savings / expected period of payment of a funded pension. The expected period of payment of a funded pension increases by 6 months every year. That is, in 2021 it was 246 months, in 2019 - 252 months. The formation of the funded part is suspended until 2021. This money is in Vnesheconombank or in a non-state pension fund. To find out how much your funded part of your pension is, you need to come to the branch of the MFC or the Pension Fund. You can also use your personal account on the official website of the department.

What will the retirement age be in 2021?

READ ON THE TOPIC:

Working pensioners will have their pensions recalculated from August 1, 2021.

Now in Russia, the retirement age for women is 55 years, and for men – 60 years.

A citizen who has reached this age limit has the right to receive a pension benefit if other requirements are met. In some cases, a person has the right to retire early. This benefit is provided to citizens who have worked for a long time in production with hazardous working conditions, civil servants, military personnel, employees of the Ministry of Internal Affairs, as well as those people who, working in difficult conditions, have lost the physical ability and professional skills to further perform their job duties. The issue of raising the retirement age has been repeatedly discussed by officials, but there has been no decision in favor of increasing the age yet. Moreover, Russian President Vladimir Putin said that no increase is planned in the next few years.

However, on May 11, the State Duma adopted in the final, third reading a bill to increase the retirement age for state and municipal workers - to 65 and 63 years for men and women, respectively.

What to do today to receive a higher pension in the future

1. Get a job officially If you officially receive the minimum salary, and everything else is in an envelope or on a card, then pension points are accrued only from the minimum wage. This means that the pension will be small. 2. Receive the maximum white salary The size of your future pension directly depends on what your official income is today. The higher the salary, the more they contribute to the budget for you and the more you will receive in old age. In 2021, a citizen can earn a maximum of 9.13 points per year. To do this, his official salary must be 87,500 rubles per month before deduction of personal income tax. There is something to strive for. 3. Save yourself Alena Putkova, specialist in creating a personal financial system “Finance is easy!”: “The pension fund of our country and any other is not intended to provide people with a happy, rich life in retirement. Let's take the International Labor Organization's Minimum Standards of Social Security Convention. It states that a pension that covers 40% of previous earnings is sufficient. This is a little more than a third. How much can you afford with this money? So the only most realistic option to receive a higher pension in the future is to take care of it yourself. Don't expect to live off the interest on your deposit. Don’t save up on this: inflation won’t let you. Therefore, we cannot do without investment.”